China’s Third Way

By Michael Pusic

Staff Writer

28/8/2020

Picture Credit: GovernmentZA

For decades, China has defied the prevailing consensus that political liberalization and economic growth go hand-in-hand. It disregards the rule of law, flouts international norms, and stifles democracy, and yet has steadily enjoyed spectacular economic growth. Most recently, the passage of the National Security Law gave Beijing the power to undermine Hong Kong’s rule of law and abridge the freedoms of its citizens, and yet this doesn’t seem to have harmed the city’s economic outlook. Many believed that Hong Kong’s British legal system, independent judiciary, and largely liberal government were instrumental in making it China’s primary financial hub. But the Hang Sang Index, which tracks the largest companies on the Hong Kong Stock Exchange, jumped by 8% in the days after the law passed and has increased by 4% over the two months since. While it’s still early days, this growth seems likely to hold in spite of Beijing’s draconian policies.

But can China sustain this apparent paradox of rapid growth under an authoritarian regime in the long run? If it can, it will overturn over a hundred years of economic and political theory, and may mark the beginning of a much darker era in history, where autocratic regimes around the world are sustained by long-term growth. But if it can’t, China will either stagnate as the USSR did, or it will erupt in the largest democratic uprising in human history.

To understand which of these outcomes is most likely, we need to delve into the logic undergirding the symbiotic relationship between political and economic institutions. Political and economic theory has traditionally held that democracy is necessary for sustained economic growth, and that high levels of growth bring about the conditions necessary for democracy.

Political and economic theory has traditionally held that democracy is necessary for sustained economic growth, and that high levels of growth bring about the conditions necessary for democracy.

The first part of this logic — that growth requires an open political system — begins with the need for a legal system. Once an economy expands beyond the point where you can know the reputation of everyone you’re dealing with, a problem arises — you don’t know if the company or person you’re about to deal with is likely to keep up their end of the bargain. This means that in order to carry out any contract, you have to sink large costs to either figure out if your potential partner is trustworthy, or hire enforcement to make sure they follow through. If the cost of enforcing a contract is too high, fewer transactions will be profitable, there will be less economic activity, and growth will slow. This is where a legal system comes in. If the state guarantees contracts, transaction costs plummet, and the economy grows faster.

Strong rule of law is somewhat opposed to autocracy, which typically rules by decree, but you could theoretically have a lawful evil dictator — one who sets laws according to his or her whim, and then sticks to them. But there are two important issues with this. First, to have long-term economic growth you don’t just need rule of law, you also need good laws. Since no bureaucracy can consistently write laws well suited to every industry, you need to open up the law-making process to the full set of stakeholders affected by the regulations. Second, businesses and investors are much less willing to make long-term investments in a country without guarantees that the ruling autocrat won’t one day seize their assets, and the only way to really assure them is to set permanent limits on the state’s power. So what began as just a legal framework necessary for economic growth ends up becoming a distinctly political one — with the government accepting limits on its power and sharing it with stakeholders.

From here, it’s not a long stretch to see how the relationship can go the other way too, with economic growth creating the conditions necessary for political liberalization. An autocratic state attempting to create a stable regulatory environment for businesses ends up binding itself to a set of rules that it is then expected to follow. If it hands control over some of these rules to citizens, it begins a cycle by which the populace expects more and more political participation. (Many thinkers, including Francis Fukuyama and Fareed Zakaria, have argued that this is how Chile democratized under Augusto Pinochet.) But even if a regime doesn’t follow this law-based path of development, many argue there are factors intrinsic to economic growth that lead to democratization. Once a citizenry’s basic needs are met and large swaths of the population rise into the middle class, they become more likely to demand greater political freedoms. Additionally, the rise of powerful businesses independent of the state can begin to curtail the government’s power by pushing for greater economic freedoms. This is arguably what led to South Korea’s democratization, and many have looked to China’s rising middle class and emerging private sector as instigators of its future political liberalization.

But China has confounded these expectations. Until recently, the Chinese Communist Party (CCP) had been reforming its economy to make it more grounded in the rule of law and to give businesses more of a say in the legislative process. According to the aforementioned theory, this should lead to more political freedom. Instead, China has clamped down on basic rights and suffocated dissent.

Shanghai

There are at least three ways this paradox can resolve itself. First, economic growth might curtail the autocratic power of the CCP, such that it’s forced to allow limited democracy — or at least relax its more draconian policies. Second, the state might fully reverse its market reforms and return to a centrally-planned economy. Third, it’s possible this framework is wrong, and China may be able to maintain the tension between a relatively open market and a closed government.

The easiest outcome to dismiss is the idea that China is on the path to democratization. In the 1990s and early 2000s, China looked like it was going to attempt to replicate Singapore’s model – enforcing stringent rule of law in economic matters, but remaining strictly authoritarian everywhere else. But as theory would predict, this soon gave rise to political liberalization. For example, the Administrative Litigation Law was passed in 1989 with the narrow aim of curbing state corruption by allowing citizens to sue government agencies for violations of existing laws. Activists used this law to bring over a million cases against the government, roughly 30% of which have been successful. In 2005, when the government narrowly eased restrictions on the media to enable it to uncover abuses of investor rights and promote more efficient markets, people used this legal framework to report political abuses and curb the state’s power. Had this trend continued, there might be a real possibility of limited democratization in China in the near future.

Unfortunately, it reversed. Chinese President Xi Jinping saw the writing on the wall, and rolled back even basic checks on his power. In 2015, he shifted away from the rule of law in favor of rule of the Party, declaring that China must “absolutely not follow the Western road of ‘judicial independence.’” Worse still, rule of Party is becoming increasingly synonymous with rule of Xi Jinping, as he abolished term limits on the presidency in 2018, and this month indicated that he plans to stay in office until death. Far from economic growth limiting his power, it seems increasingly likely that the economy will become an instrument of President Xi’s will.

Given this, let’s look at the second possible outcome – that China regresses to a Maoist, centrally-planned economy. Over the past few years, Xi has pushed a massive wave of mergers to increase the size of state-owned enterprises (SOEs), prompting the absorption of many private firms and increasing the role of the state in various industries. To finance these acquisitions, lending has been redirected from private firms to SOEs, so much so that the amount of lending available to the private sector has shrunk 80% in the past seven years. This expansion of the state’s role in the economy is likely to be accelerated by Xi’s Made in China 2025 plan, which aims to transition the economy from basic manufacturing towards high-tech innovation across 10 key industries; in four of these industries, SOEs have a revenue share of 83%. All this suggests a shift towards a more state-run economy.

But if Xi does pursue anything near a full return to Maoism, we are likely to see a significant slowdown in growth. Nicholas Lardy, a US economist, estimates that the aforementioned decreases in private investment alone are already pulling the nation’s GDP growth down by as much as 2%. Part of the reasoning behind this is pretty straightforward — SOEs are just much worse companies than their private counterparts. By the Chinese Ministry of Finance’s own calculations, more than 40% of these firms consistently operate at a loss, and since the merger frenzy began, their return on assets has nearly halved. As these firms become more inefficient and bloated, they will attract fewer customers and capital, their growth will stall, and the trend of rising wages and falling poverty will begin to slow or even reverse.

But there is also a deeper and more complex reason why China won’t be able to sustain its current growth with a state-run economy. For the past 40 years, its economy has grown because its low wages gave it a comparative advantage in basic manufacturing. But foreign firms have now bid up wages to a point where China can no longer compete with poorer nations on low-cost production. Instead, it will need to compete with richer countries on the quality of its innovation and technology; it needs to shift from producing to designing products. And while SOEs could handle low-cost manufacturing, they are structurally incapable of producing this kind of innovation. A huge number of studies have established that the greater a state’s ownership of a company, the less it invests in research and development and the fewer patents it produces. The logic behind this is complex, but essentially government bureaucrats are likely to protect bloated firms against more innovative competitors for many reasons (including saving jobs). This means that SOEs have no incentive to innovate because they don’t face the threat of obsolescence, and private firms don’t innovate either because, even if they come up with better or cheaper products, the state will intervene to protect the SOEs.

If China elects to regress to central planning, we will likely see the stagnation of the world’s second largest economy within the next decade. It is possible that President Xi will accept this as the price of maintaining political control, but it seems more likely he will try to maintain high levels of growth even as he increases the state’s role in the economy. That is, he will likely pursue a third way, in which key elements of an open economy are adopted but directed according to the state’s autocratic ends. To pull this off, he will need to manage two Herculean feats. First, he will need to find a way to harness the efficiency and innovation of private firms, while still keeping them within state control. Second, he will need to create an economic environment for these private firms to grow, which allows for predictability and low transaction costs, but which doesn’t rely on an open political system.

Factory in Shenzhen (Picture Credit: Steve Jurvetson)

President Xi seems to be making real progress on the first of these challenges by fostering the growth of a new type of firm which operates entirely independently on a quarter-to-quarter basis, but which remains within the state’s control. The actual mechanics of this are hugely varied, and likely to become even more diverse. The state may allow companies to operate independently most of the time, but pass laws to compel their cooperation in particular areas, like the 2017 National Intelligence Law. Or it can exercise control by punishing top executives with jail time for disobedience, like when it imprisoned the chairman of the Anbang Insurance Group for fraud after he ran afoul of the party. Even with the most traditional SOEs, the CCP will often retain a controlling share in the firm, but dilute its ownership by listing the company on foreign stock exchanges or by forming joint ventures with foreign firms to introduce greater discipline on the company’s operations. The only common feature of this new kind of state governance is that it keeps the company at a greater distance, and so allows the market to guide more of the firm’s decisions.

President Xi seems to be making real progress on the first of these challenges by fostering the growth of a new type of firm.

This approach solves a lot of the problems of state-ownership. When firms are privately owned or traded on foreign stock exchanges, capital ceases to be allocated on the basis of political expediency, and starts flowing to those firms most poised to take advantage of it. Obsolete companies fail sooner, and their more innovative competitors grow faster. The day-to-day managers of these firms are no longer selected by bureaucrats, but are instead chosen by shareholders who have the knowledge and incentives to effectively govern the firm. Companies become leaner and more innovative, all while remaining within government control.

But the second challenge remains: even fully private companies might not be able to actively innovate and grow without the infrastructure of an open political system. If these firms don’t have the assurances of strong rule of law, they may end up having to shoulder the immense burden of enforcing their own contracts. And they may pay dearly for the insecurity intrinsic to operating within a market that exists at the whims of a dictator rather than within the bounds of constitutionally-assured economic rights. The final, and most pressing question is whether President Xi will be able to meet these market needs — predictability and low transaction costs — without acquiescing to the open political system they are typically tethered to.

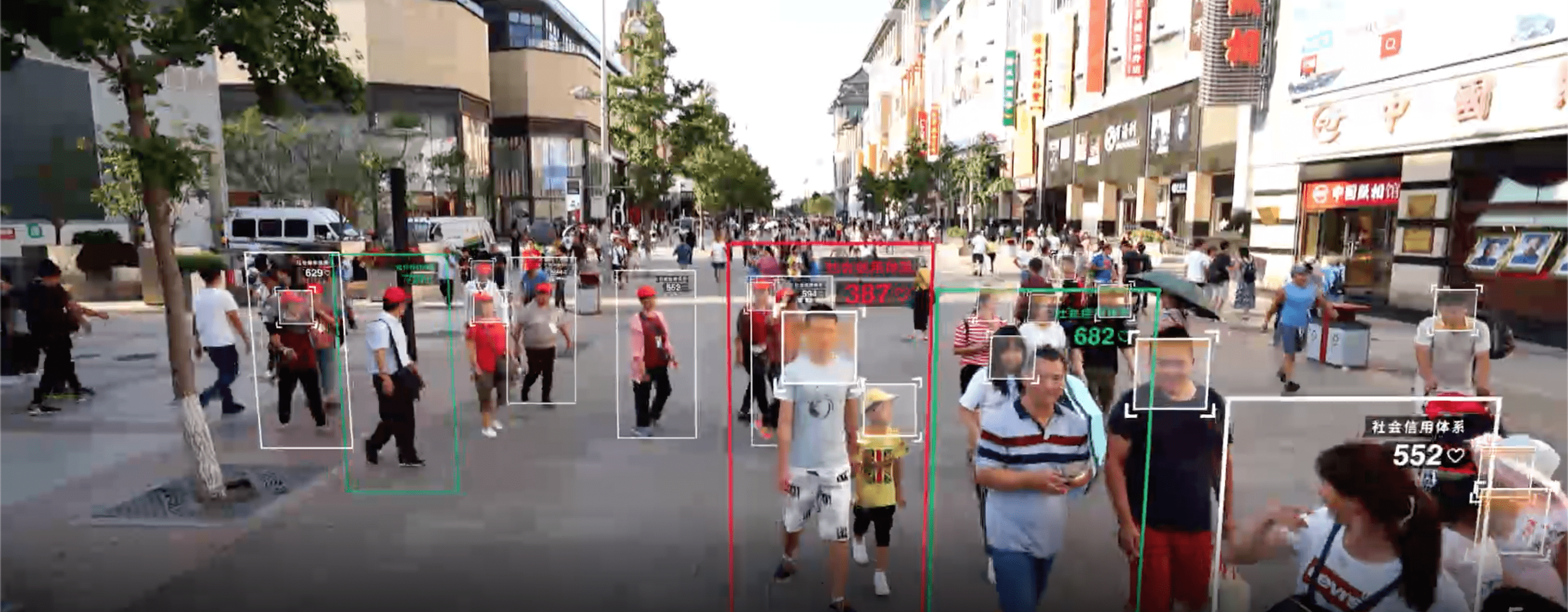

By the government’s own statements, China’s Social Credit System (SCS) constitutes an attempt to lower transaction costs without submitting to the rule of law. The guiding idea is that transactions can be ensured either by force or by trust. Rule of law functions by threat of force, but the SCS operates by attempting to quantify trust. That is, it provides a quantitative metric of the trustworthiness of every business and citizen in China. The scores are based on a huge, Orwellian database that monitors most citizens 24 hours a day through internet activity and surveillance cameras, and then uses AI to process their every action into a single score that is constantly updated. Firms and people no longer have to worry about getting scammed, not because the state has bound itself to intervene if they are, but because they now have a way to assess who is trustworthy. Since 2014 the SCS has been piloted in different parts of China, and this is the first year it has been fully operational. So far it seems to be working — from 2014 to 2019 China jumped from the 29th to the 14th most innovative economy and, according to the World Bank, is among the top 10 countries most quickly improving their environment for business.

Picture Credit: ABC News

There’s been a lot of talk about the dangers the SCS poses, but the most pressing threat is actually the economic prosperity it might bring about. Rule of law has long stood as one of the strongest tethers between prosperity and democracy. If the SCS succeeds, it will not only sever this link, but create a system in which growth actually depends on an autocratic regime. The more popular and refined the SCS becomes, the more growth it will bring about, and the more unilateral power the state will have to shut citizens out of its economic system. The criteria for this metric is unilaterally decided by the state, which allows them to punish individuals for anything that might lead to democratization – publishing articles, attending protests, even just speaking to friends who criticize the state. Individuals with low scores are already unable to book train tickets, hotels, or use social media. They are excluded from the best universities, housing, and even healthcare. As the metric becomes more entrenched in the country’s economic system, the state will gain ever more power to snuff out citizens’ yearnings for basic rights and freedoms.

If the social credit system succeeds, it will not only sever this link, but create a system in which growth actually depends on an autocratic regime.

It’s worth noting that even if the SCS fails, there may be other ways to lower transaction costs while maintaining an authoritarian regime. As mentioned, Singapore has managed to marry rule of law on economic matters with authoritarian rule on all political issues. At the turn of the 21st century, China tried and failed to replicate this. The reasons for this failure are complex, and involve deep cultural and historical differences between Singaporeans and Chinese people; Singapore has a long-standing tradition of private property rights and markets going back to its status as a British colony, while China, since the Communist takeover, has only had codified property rights since 2007. The total population of Singapore is also smaller than that of Hong Kong alone. But Singapore still proves that it is possible to have limited rule of law and explosive economic growth under an autocracy. And if the SCS should fail, there is a good chance the CCP will try again to replicate this model, potentially with greater success.

Singapore Supreme Court. Singapore has managed to marry rule of law on economic matters with authoritarian rule on all political issues. (Picture Credit: Terence Ong)

Finally, there’s the issue of the CCP providing predictability without setting permanent limits on its power. How can it assure investors that it will protect private property rights without ever committing itself to do so? For emerging economies, this question has to be answered in comparative terms. Any nascent government — democratic or autocratic — faces real challenges in assuring companies that it will protect their rights. As much as autocrats might nationalize a company for their own benefit, a new democracy might be overwhelmed by a wave of populism and seize an entire industry. Given this, an autocrat who consistently acts to promote relatively open markets, protects private property rights, and generally avoids unpredictable behavior can actually provide more stability than a nascent democratic regime, whose leadership changes every few years. Take Botswana and Singapore, which gained independence within a year of each other. Botswana has a thriving democracy, rich natural resources, and the least corruption in Africa, and yet has a GDP per capita of just $8,258, an extreme poverty rate of 16%, and minimal foreign direct investment outside of its diamond industry. Singapore has no natural resources and a brutal autocracy, and yet has a GDP per capita of $65,233 and virtually no poverty. There are many reasons for this difference, but at least one is that Singapore has enjoyed a stable regulatory environment since it gained independence, while Botswana’s has vacillated every few elections. To replicate what Singapore achieved, President Xi would need to begin behaving in far more predictable, economically beneficent ways, and would need to put in place a seamless succession plan. But if he does, he may be able to provide more predictability than even mature democracies.

Whether China manages to marry a relatively open market to a closed government is therefore contingent on many things. It must abandon inefficient SOEs in favor of more independent, mixed-ownership firms. It must strike the right balance between the competing impulses of state control and business independence. The SCS, a system that, while promising, has only become operational this year, must be up to the task of managing the Chinese economy. And finally, Xi Jinping will need to sort out a clear line of succession. If China manages to do all these things – and that’s a very big “if” – it will truly have pioneered a new political and economic model.

Above all, we have to remember that modern economic growth is only about 200 years old. To think that the West has discovered the only way to achieve growth, and that it is inexorably tied to political freedom and democracy, smacks of extreme naïveté. Much research has already found that no single legal system promotes growth universally around the world, so it’s odd to think that only one kind of political system can do so. It seems far more likely that many paths to prosperity will be discovered, some of them linked to democratic governance, and others bolstered by tyrannical regimes. And while China figures out its distinct path to wealth, it will have many ways to incentivize businesses to stay invested in it. If nothing else, it controls access to 1.2 billion consumers, and can remove obstructions to progress far more easily than any democracy can (e.g. by razing neighborhoods, crushing strikers, suppressing wages – and eliminating anyone who disagrees).

What might a successful Chinese third way look like? Imagine it’s 2060. China has managed to escape the middle-income trap without democratizing, and now has an economy that operates as efficiently as America’s or Germany’s, fueled by about a billion workers, which feeds directly into the unchecked power of the state. A regime like this would be capable of unimaginable levels of oppression. We could see things like the Uyghur concentration camps expand, the rise of a surveillance state that makes dissent impossible, and a new global order shaped by a country that doesn’t even pretend to care about human rights. Such a regime would inspire others, and would be able to share innovations in authoritarian governance with friendly tyrannies around the world. We would see the fall of the liberal order, and the dawn of a much darker chapter in human history.

Atushi City Vocational Skills Education Training Service Center, a detention camp, in Xinjiang

For decades, Western policymakers have abetted China’s economic growth under the assumption that this would bring about political liberalization. This logic shaped the US’ China policy until the Obama administration, helped arrange China’s acceptance into the WTO, and contributed to a number of loans from the World Bank. This strategy was wrong. By including China in the global order, the West has only accelerated the growth of a regime that ultimately hopes to combine the most oppressive aspects of autocracy and capitalism. China is now less likely to democratize than ever. Political change will come only through sustained pressure from within and without. We can no longer wait complacently for China’s wealth to bring freedom to its people.

Share Me

Tweet Me

Mail Me